AI-powered real estate platform · Just ask. Unrealty will find it.

Find whereyou'll live next.

[ 2 ]AI Design

Visualise your future home with AI-powered interior design. See any room transformed before you move in.

AI visualisation

[ 3 ]Neighborhood OFFERS

Start exploring today and make your neighborhood feel more like home!

Discover Your TOP Neighborhood OFFERS

[ 4 ]interactive map

Explore properties on an interactive map and find the perfect neighbourhood for you.

Discover Your BEST LOCATION

[ 7 ]features

AI-powered tools to make your property search smarter and faster

Features by Unrealty

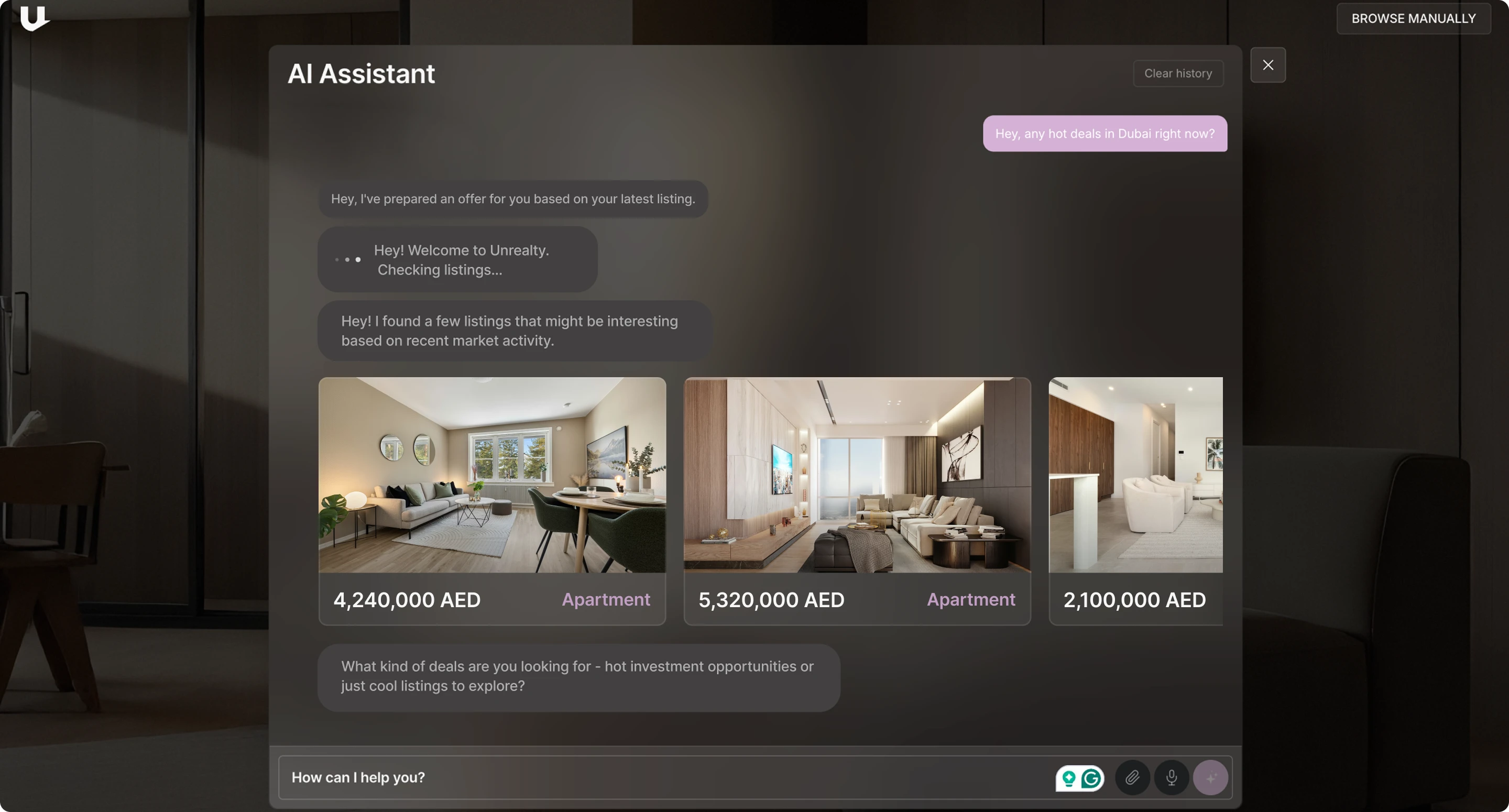

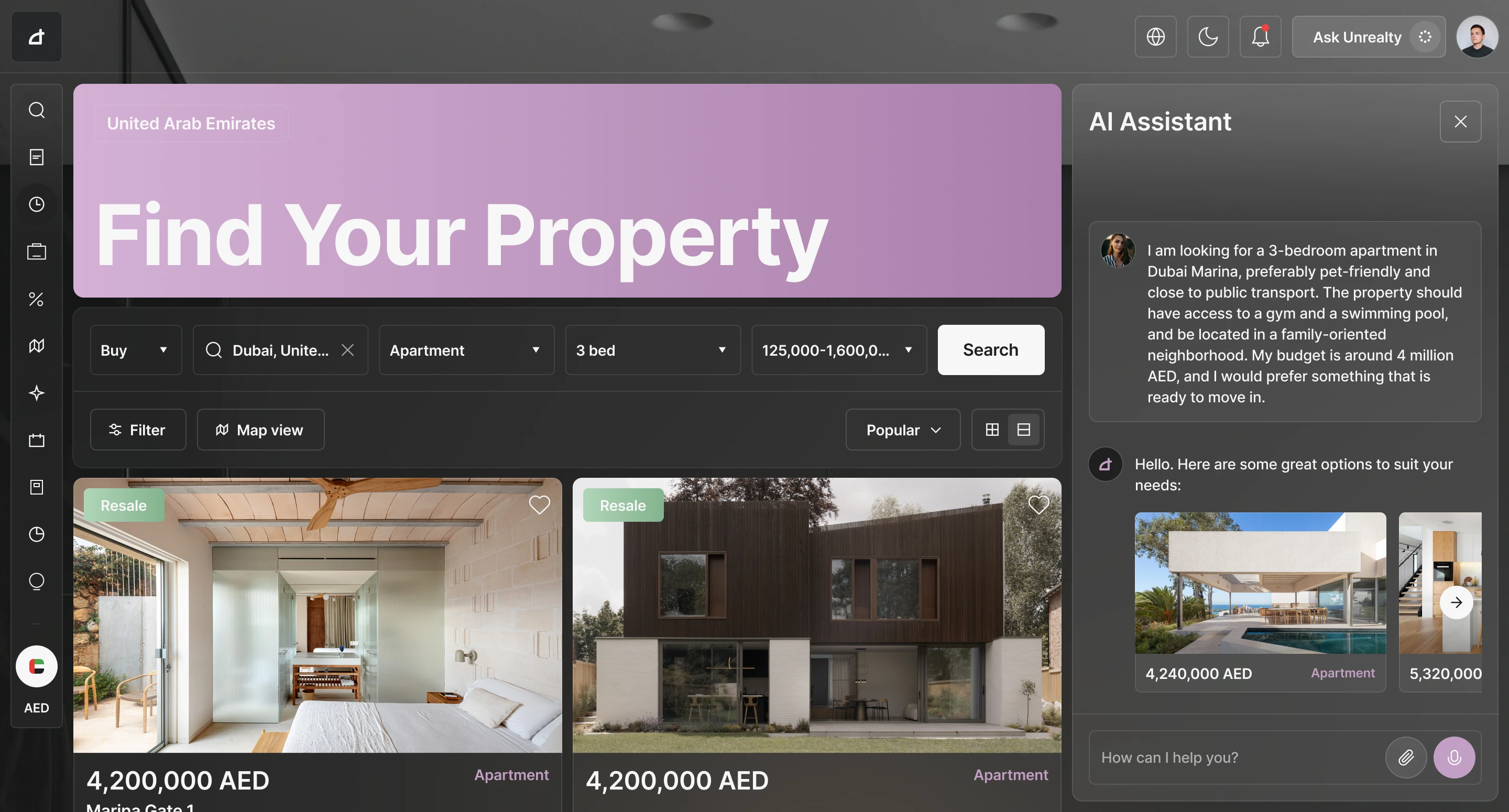

AI Assistant

AI Assistant Listings

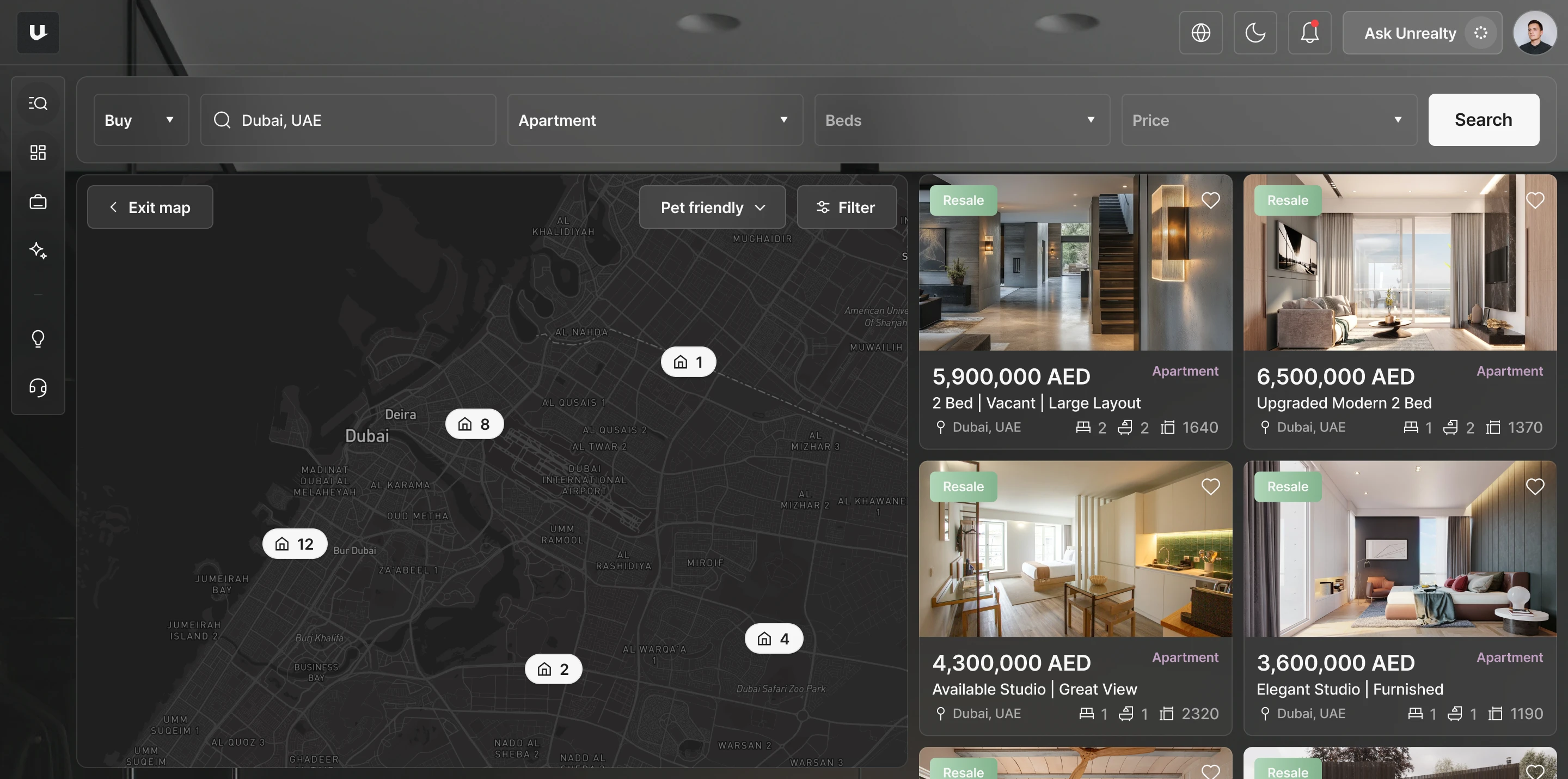

Listings Map

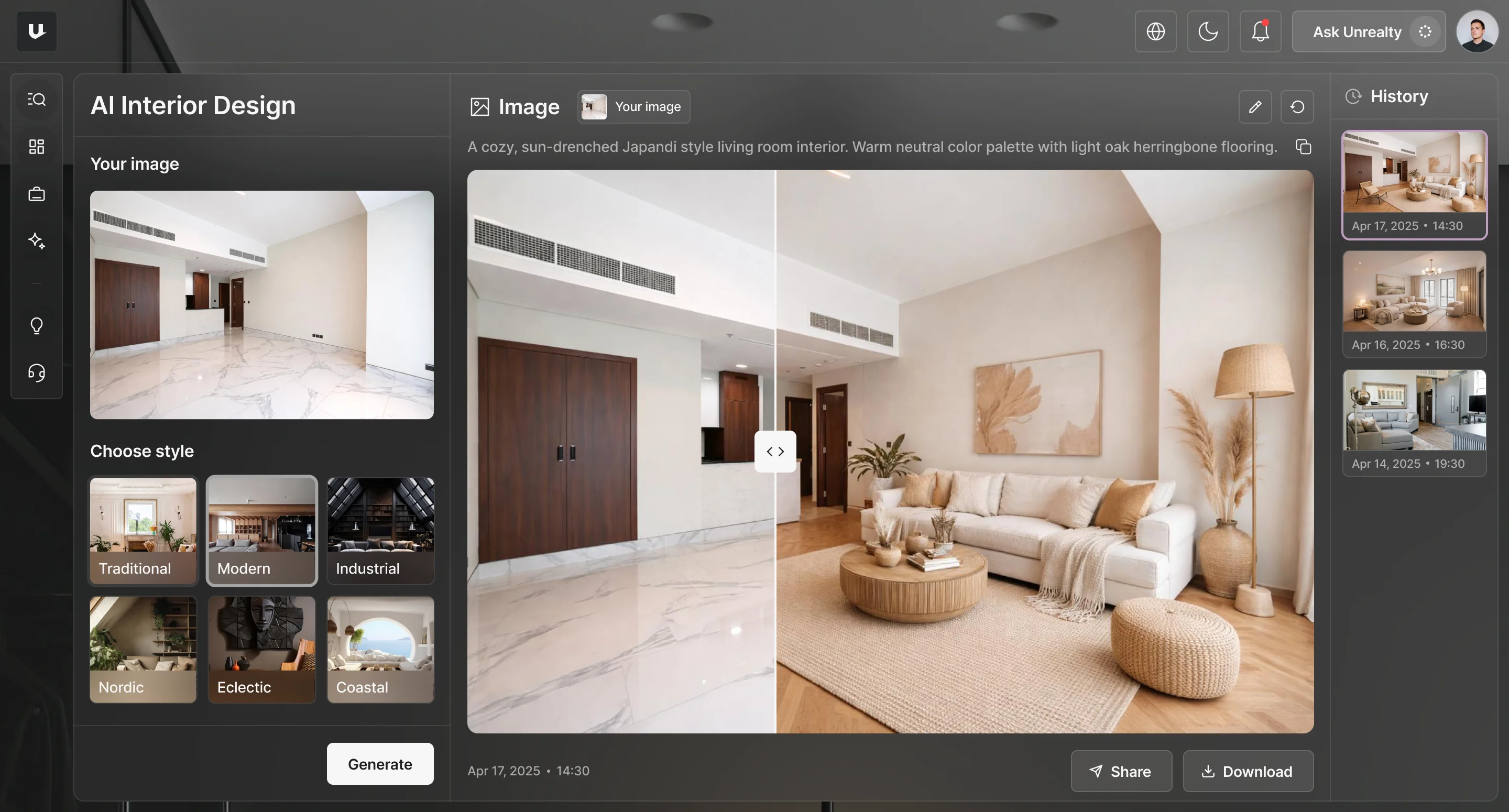

Map AI Interior Design

AI Interior Design Analytics

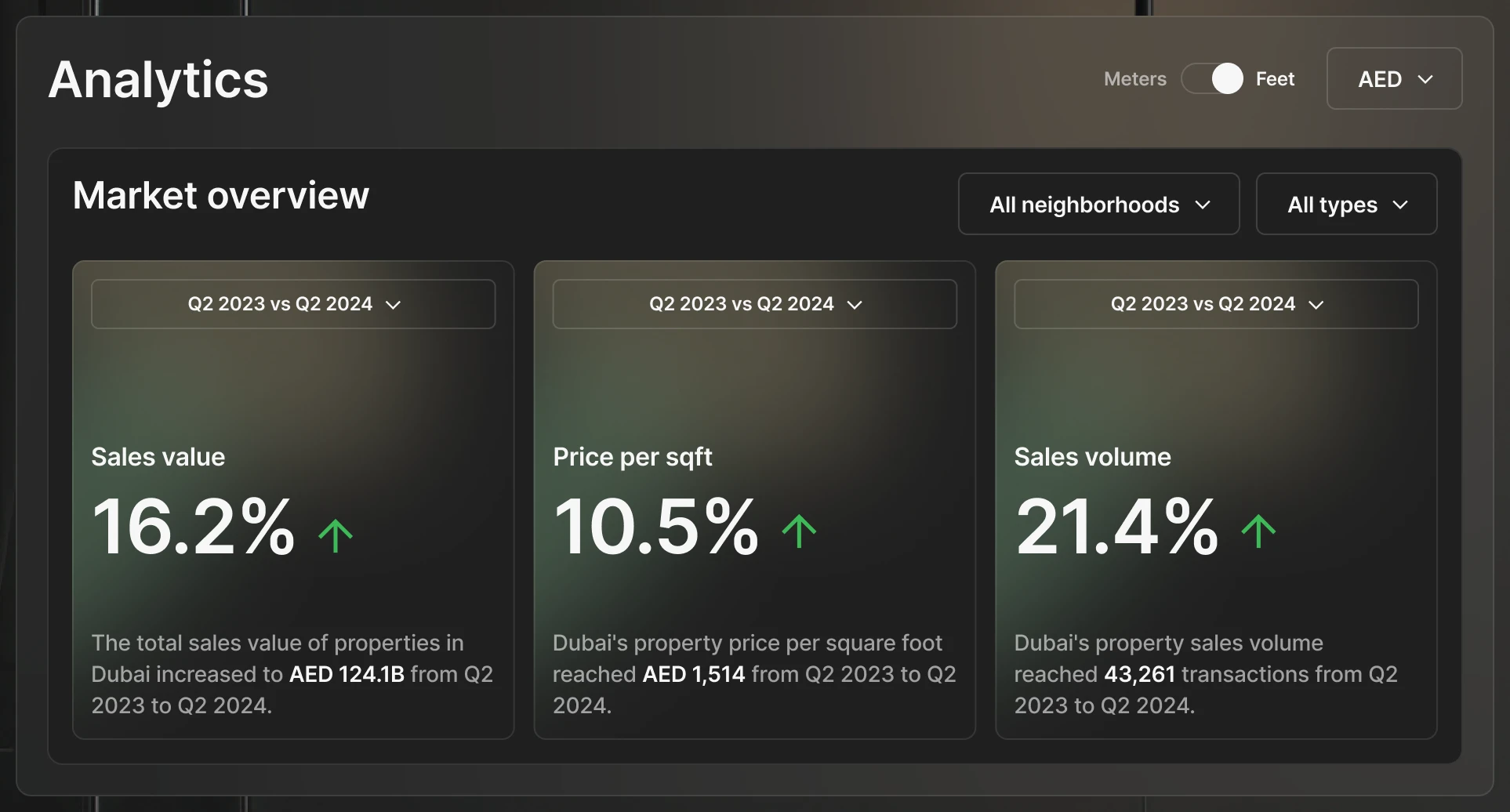

Analytics

across 2 countries

AI Assistant

Your intelligent real estate companion that helps you find the perfect property effortlessly.

across 2 countries

Listings

Manage and showcase your property listings with beautiful, professional presentations.

across 2 countries

Map

Explore properties on an interactive map with satellite views, community overlays, and neighbourhood insights.

across 2 countries

AI Interior Design

Reimagine any space with AI-powered interior design that transforms empty rooms into beautifully staged properties.

across 2 countries

Analytics

Data-driven market insights and trends to help you make smarter investment decisions.